How Vertical Integration Shapes Innovation

The way firms are structured can influence whether innovation comes from the top or from the factory floor.

. National Gallery of Canada, Ottawa. © 2020 Judd Foundation / Artists Rights Society (ARS), New York")

In part one of this series, I took a look at how frontier firms in the tech and auto sector are turning to vertical integration. But this shouldn't suggest that vertical integration is a rising trend in all sectors or country-contexts. In this post, we'll take a look at how vertical integration fosters certain types of innovation over others.

The original rationale for vertical integration was to control as many stages of the value chain as possible to maximize margins. Every step in the production process—from raw materials to processing, from finished good to distribution—introduced an intermediary, each shaving off some margins off the final profit. So, by consolidating these steps in-house, firms could eliminate middlemen and capture more of the profit themselves.

But this logic shifted with globalization. As access to international markets expanded, firms discovered new pockets of productive capacity in regions with cheaper labor and more relaxed regulations. Fragmenting supply chains and outsourcing production became a new way to cut costs as it allowed Western firms to benefit from lower labor costs abroad.

But if the initial impetus to offshore and fragment production was to give multinationals access to cheaper labor costs in the Global South, then Chinese firms, already at the center of these cheaper supply chains, can now gain a new edge by vertically integrating themselves. This is in fact part of the reason why BYD has bested Tesla with its unbeatably low prices (a function of scale economies and vertical integration).

Yet while vertical integration is increasingly common in places like China, with firms like Tongwei Solar in solar PV manufacturing or Huawei in consumer electronics and tech services more broadly (especially with their recent advances in semiconductor production), the neo-Fordist shift is also gaining traction in parts of the West, even where the cost advantages of integration are missing. What gives?

Aside from creating more resilient supply chains in the face of global disruptions and rising geopolitical tensions, vertical integration may be increasingly important in sectors where process innovation (rather than product innovation) is critical.

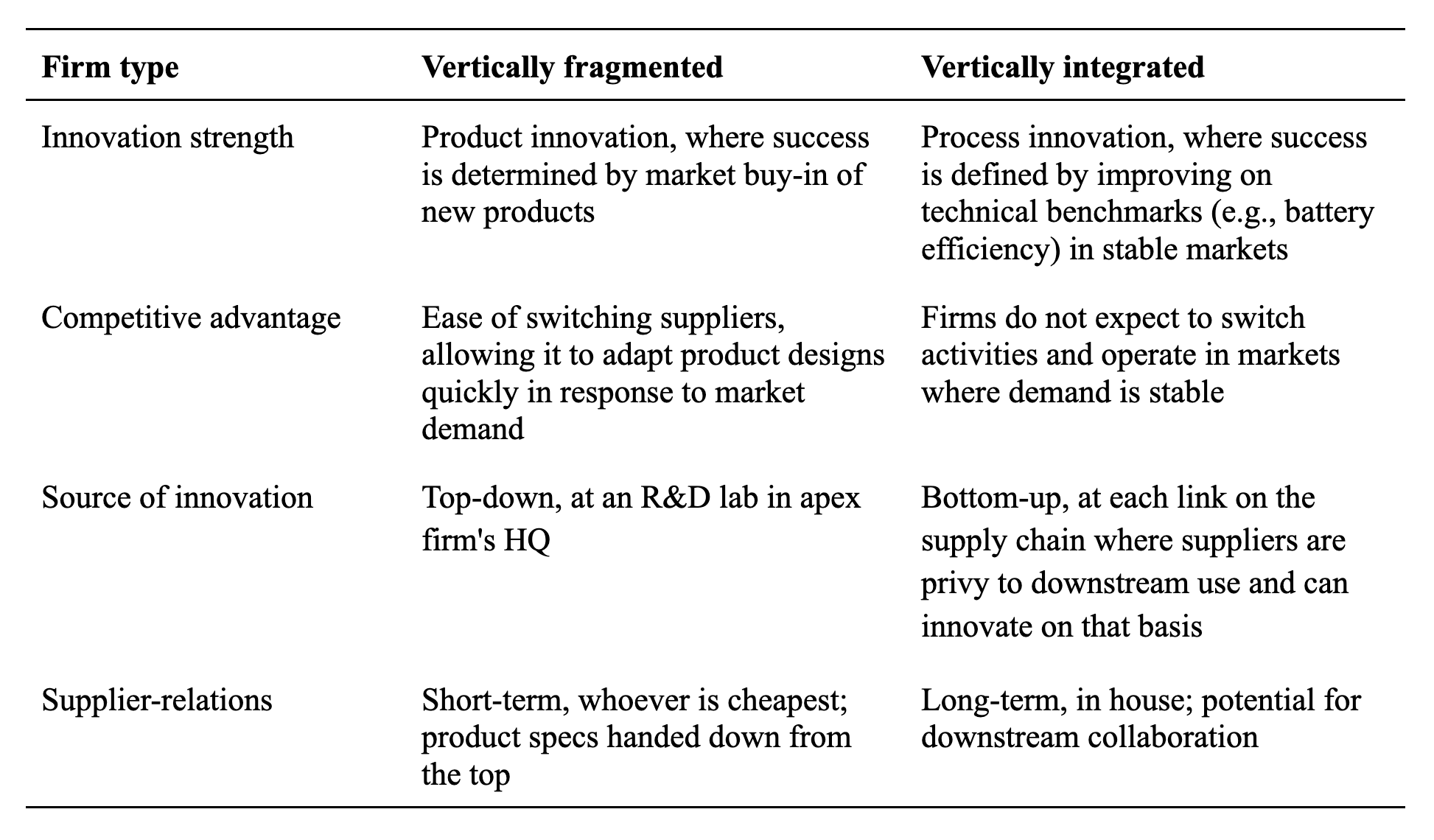

Product innovation in vertically fragmented firms

First, let us begin by looking at the complementarity between vertically fragmented firms and product innovation. That is, innovation that focuses on developing new features, services, or user experiences. In this model, technological innovation is decoupled from production. The apex firm dictates design and product changes, often resulting in entirely new supply chains. This structure rewards flexible value chains where disposable, market-mediated relationships with suppliers is an advantage.

Take, for example, a toy brand that frequently rolls out new product lines, each requiring different materials and manufacturing processes. For such firms, short-term, transactional relationships with manufacturers gives them the flexibility in toy design that underpins their strategic advantage.

Fragmented value chains do not eliminate innovation entirely. Firms lower in the chain may compete on production efficiency, offering downstream customers more cost-effective options. And because each layer of the supply chain is exposed to market discipline, suppliers may can outcompete each other by seeking improvements in the production process. However, this type of innovation is limited to cost reduction or incremental process improvements. The apex firm maintains control over the product design and sets the specifications that manufacturers must follow. As a result, improvements in the production process do not improve the final product outside of reducing its price.

In firms optimized for product innovation, the primary benchmark for success is consumer uptake. Innovation is seen as originating from formal R&D units rather than the factory floor. In this view, once a new technology is developed, it can be deployed across firms and geographies with minimal friction, regardless of where production takes place. And so offshoring manufacturing is not considered a barrier to innovation or organizational learning, but a cost-saving strategy since production is treated as disjointed from technological advancement. Accordingly, policies to promote innovation tend to focus on strengthening intellectual property rights or subsidizing investment in upstream knowledge inputs like R&D and higher education.

Process innovation in vertically integrated firms

Vertically integrated firms, by contrast, are better positioned to reap the benefits of process innovation, which is all about improving how things are produced. This includes new production techniques or engineering improvements on the factory floor. Process innovations are discovered through hands-on experience with the materials, tools, and workflows involved with production—what the economist Kenneth Arrow called learning by doing.1

In sectors where advances in production establishes a firm’s competitive advantage (such as semiconductors, solar panels, or batteries) there tends are clear technical benchmarks for success (smaller chip sizes, higher energy efficiency, or greater storage capacity). This is crucial because it makes process innovation measurable. This means that manufacturers are not only expected to improve yield and reduce costs, but also to innovate in their production processes in order to push the boundaries of these technical benchmarks.

It’s important to recognize not just how innovation happens, but where it takes place. In sectors driven by product innovation, breakthroughs often come from R&D labs, typically within the apex firm. But in production-oriented industries, innovation frequently emerges from within the value chain itself. This matters because changes in one stage of production can ripple through the entire value chain. For instance, a new material used in a single component might compel downstream changes such as in the products final design. It might also require different upstream inputs.2

In this model, innovation can emerge at any point along the value chain. And rather than allowing these production-based insights to remain siloed at the supplier level, vertically integrated firms are able to capture and leverage them. On top of that, owning the value chain means they can better coordinate across it, putting them in a stronger position to translate localized improvements into system-wide gains.

In both vertically fragmented and vertically integrated firms, process and product innovation are possible. However, each organizational model better complements a particular type of innovation. The ability to coordination across the value chain in vertically integrated firms fosters process innovation. Conversely, the flexibility afforded by transactional supplier relationships in the fragmented model allows the apex firm to rapidly adjust designs, naturally complementing product innovation.

The return to process innovation

As discussed in my piece on the evolution of firm strategies, many frontier firms in the West have systematically prioritized product innovation. They have poured resources into R&D, branding, and product design, while largely outsourcing the production process itself—often to lower-cost regions like China.

This shift wasn’t just about cost savings. It reflected the type of innovation these firms chose to prioritize and the belief that innovation occurred not on the factory floor but in the R&D lab. Not only that, but by focusing on knowledge-intensive production, firms could avoid the capital and labor costs of production and generate steady high-margin rents from licensing, patents, and other intellectual property. All this has made many Western multinationals, from Nike to Apple, fabulously profitable. However, by offshoring production, these firms also created the conditions for countries like China to move up the value chain and become leaders in process innovation

In the United States, industrial policy over the past several decades has aligned with this approach to innovation. Support was largely directed toward upstream research and early-stage technologies.3 Agencies like DARPA played a central role, backing breakthroughs such as the internet, GPS, and drone technology. Meanwhile, little attention was paid to production capabilities or manufacturing infrastructure. It wasn’t until the recent passage of the CHIPS and Science Act and the Inflation Reduction Act that American industrial policy began to re-engage with the production side of the economy.

Vertical integration is not merely a return to past organizational practices. It represents a renewed effort by frontier firms to gain a competitive edge through process innovation. Whether this trend remains confined to leading companies or evolves into a broader restructuring of capitalism is an open question. Either way, the resurgence of vertical integration should be a reminder that innovation comes not only in R&D labs but also from production on the factory floor.

See: Arrow, Kenneth. 1962. “The Economic Implications of Learning by Doing.” The Review of Economic Studies 29(3): 155–73.

For more, see: Chang, Ha-Joon, and Antonio Andreoni. 2020. “Industrial Policy in the 21st Century.” Development and Change 51(2): 324–51.

See: Block, Fred. 2008. “Swimming Against the Current: The Rise of a Hidden Developmental State in the United States.” Politics & Society 36(2): 169–206; and Wade, Robert H. 2017. “The American Paradox: Ideology of Free Markets and the Hidden Practice of Directional Thrust.” Cambridge Journal of Economics 41(3): 859–80.

Deverticalisation corresponded with a lot of economic & political changes. The thrust was financial rather than strategic? Govt spending under Reagan (the tax cuts) effectively saw hoarding of business savings rather than R&D spend. This was a fundamental economic shift accompanied by the primacy of shareholder value. The most important aspect of SV was (supposedly) to resolve the principal agent problem of manager led companies by distributing cash to owners to invest as they saw fit. Companies that wanted to maintain R&D & verticalisation (I disagree with the characterisation of labs in modern companies btw) then became prey to junk bond / private equity merchants. While I like this piece, I feel it misrepresents the drivers of change. These decisions were not about competitive advantage or innovation. They were about a switch to speculation driven rather than fundamentals driven capitalism. Once executive pay was tied to stock price, the deal was done. Verticalisation nowadays is again non strategic but political. It remains to be seen where it leads but as demand has dried up in the West, it is hard to see how product innovation will offer competitive advantage in markets selling to over-leveraged, under-waged Americans. You are right to identify the shifts but presenting this is as purely ‘rational’ / strategic market driven behaviour feels unhelpful. The shift was away from fundamentals driven capitalism (lab, product, process, customer) to financialisation (offshoring, market power, de-skilling, stock market).